Will Motor Insurance Become Cheaper Under IRDAI's 2026 Reforms?

IRDAI's 2026 reforms could reshape motor insurance in India. Explore how Bima Sugam, usage-based policies, EV insurance, and regulatory changes may impact premiums, claims, and policyholders.

By Swati Tomar

Jun 01, 2026 06:11 am IST

Will motor insurance finally become cheaper or are Indian drivers about to pay even more?

It's a question many vehicle owners are asking as motor insurance premiums continue to rise alongside fuel costs, maintenance bills, and spare-parts prices. For motorists already feeling the pinch of higher ownership costs, any talk of IRDAI motor insurance reforms naturally raises hopes of lower premiums.

That's exactly why IRDAI's 2026 reform agenda is attracting so much attention.

From a new digital insurance marketplace and stronger consumer protections to the rise of usage-based insurance India, the regulator is pushing changes that could reshape how motor insurance is bought, priced, and serviced in India.

But here's the catch: these reforms aren't really about making insurance cheaper overnight.

They're about making the system more transparent, competitive, and efficient. And if that happens, lower costs could eventually follow.

The bigger question is whether these changes will genuinely benefit vehicle owners, or simply change the way insurance works. That's where the real story begins.

Will Motor Insurance Premiums Reduce in 2026?

The short answer is: probably not immediately.

While IRDAI's motor insurance reforms aim to make motor insurance in India more transparent, competitive, and consumer-friendly, rising repair costs, increasing claim payouts, and higher vehicle complexity mean car insurance premiums may not fall in the short term.

However, drivers could benefit from easier vehicle insurance renewals, improved claim settlement experiences, better pricing transparency, and more personalized motor insurance policies over time.

In simple terms, the reforms are more likely to improve value than deliver an instant reduction in premiums.

What Are IRDAI's 2026 Motor Insurance Reforms?

IRDAI's recent initiatives are not centered around a single policy change. Instead, they form part of a broader effort to modernize India's insurance ecosystem and improve customer experience.

Some of the most significant developments include:

Reform | Impact on Vehicle Owners |

Bima Sugam platform | Easier comparison of motor insurance policies |

Faster grievance resolution | Improved customer support |

Greater insurer accountability | Better claims experience |

Digital insurance infrastructure | Less paperwork and quicker servicing |

Usage-based insurance products | Potential savings for low-mileage drivers |

Increased competition | Greater transparency and product innovatio |

Taken together, these reforms could transform how Indians buy, manage, and renew their motor insurance policies.

The Real Question Isn't Just About Price

When most people hear about insurance reforms, they immediately think about one thing: lower premiums.

That's understandable.Vehicle ownership is becoming increasingly expensive, and insurance is a mandatory cost that every vehicle owner must bear.

But IRDAI's reforms aren't primarily designed to slash prices.

Instead, they aim to address long-standing issues such as:

Complicated policy comparisons

Poor transparency

Delayed grievance handling

Inconsistent claims experiences

Excessive paperwork

In many ways, the regulator is trying to make motor insurance work better before making it cheaper.

Why Car Insurance Premiums Keep Rising?

To understand whether motor insurance can become cheaper, it's important to understand why costs have been increasing.

Today's vehicles are far more sophisticated than they were a decade ago.

A minor collision can now involve:

Cameras

Parking sensors

Radar systems

LED lighting

ADAS components

Electronic control units

Even relatively affordable cars now feature technologies that increase repair complexity and replacement costs.

The growing popularity of SUVs and EVs has further increased claim costs for insurers.

Rising third-party insurance liabilities, inflation, and expensive spare parts continue to put pressure on motor insurance premiums.

As a result, dramatic reductions in car insurance premiums remain unlikely in the near future.

What Is Bima Sugam and Why Does It Matter?

Among all the reforms, Bima Sugam could have the most visible impact on consumers.

The platform is expected to function as a centralized digital marketplace where customers can compare, purchase, renew, and manage insurance policies from multiple insurers through a single interface.

Think of it as bringing the convenience of online travel booking platforms to insurance.

For consumers, this could mean:

Easier policy comparison

Better premium transparency

Reduced paperwork

Faster renewals

Improved access to policy information

The Bima Sugam platform could also encourage greater competition among insurers, making it easier for customers to identify the best-value policies.

Could Insurance Companies Pass Their Savings on to Drivers?

One of the less-discussed aspects of IRDAI's reforms involves reducing inefficiencies across the insurance value chain.

A portion of every premium goes toward:

Distribution costs

Agent commissions

Administration

Documentation

Customer acquisition expenses

Digital platforms and standardized processes can reduce many of these costs.

If insurers become more efficient and competition intensifies, some of those savings could eventually benefit consumers.

However, any meaningful impact on premiums is likely to happen gradually rather than immediately.

Also read: 7 Reasons Your Bike Insurance Costs More Than Your Friend’s for the Same Bike

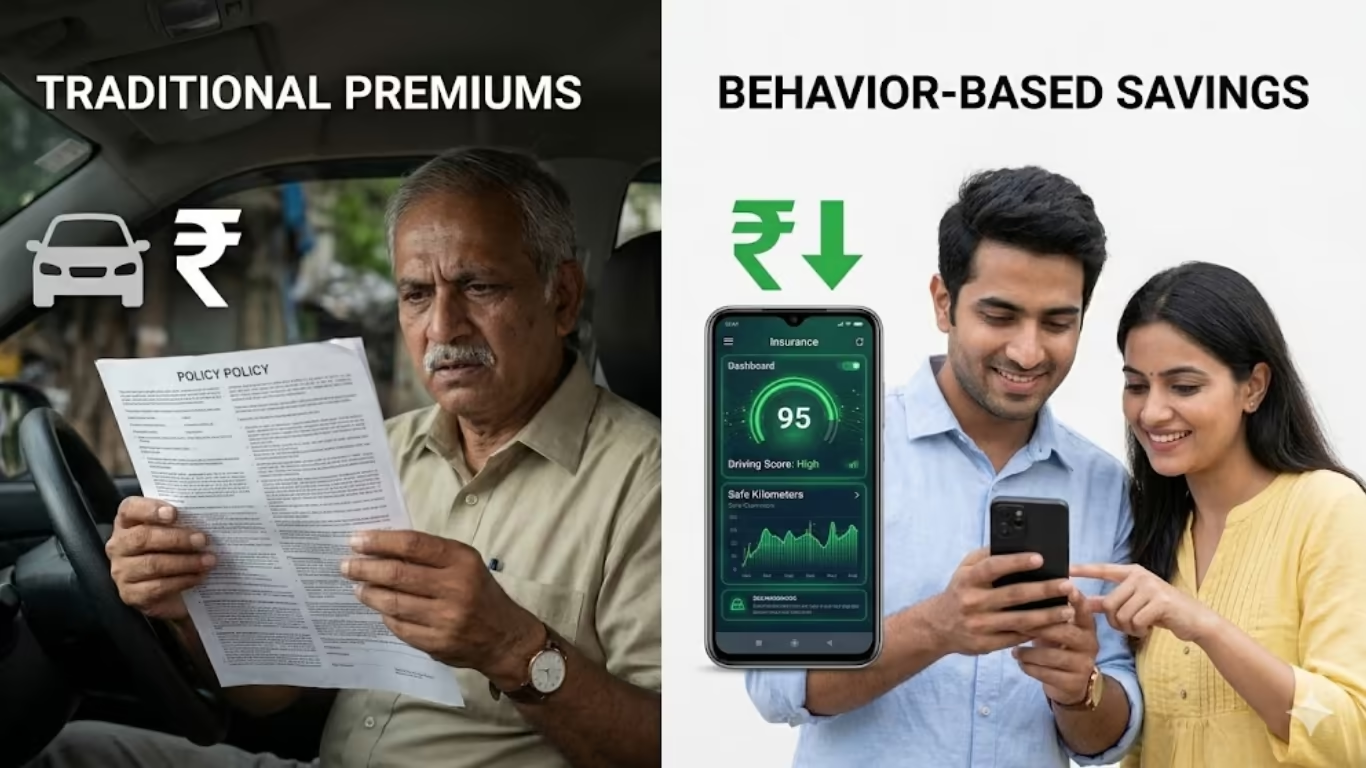

Could Your Driving Habits Affect Your Premium?

One of the biggest long-term shifts in motor insurance could be personalized pricing.

Traditionally, premiums are based on factors such as:

Vehicle type

Location

Vehicle age

Claims history

But future insurance products may increasingly consider how a vehicle is actually used.

This is where usage-based insurance India comes into the picture.

Potential products include:

Pay-as-you-drive insurance

Pay-how-you-drive insurance

Distance-based premiums

Safe-driving rewards

For motorists who drive less frequently or maintain safer driving habits, usage-based insurance could eventually result in lower premiums.

How Will IRDAI Reforms Affect EV Owners?

Motor insurance is evolving at the same time India's EV market is expanding rapidly.

Unlike conventional vehicles, EVs derive a significant portion of their value from battery systems.

Yet many consumers still assume standard insurance policies fully address battery-related risks.

Before renewing an EV insurance policy, owners should ask:

Is accidental battery damage covered?

What depreciation rules apply to battery replacement?

Is charging equipment covered?

Are battery protection add-ons available?

As EV adoption increases, insurers are expected to introduce more specialized EV insurance products designed specifically for electric vehicle ownership.

From an automotive perspective, this is one of the most important insurance trends to watch over the next few years.

The Biggest Benefit Might Not Be Lower Premiums

If there is one area where consumers could notice improvements relatively quickly, it is claims servicing.

Historically, claims experience has been one of the biggest pain points for policyholders.

IRDAI's reforms place greater emphasis on:

Faster complaint resolution

Better digital servicing

Improved transparency

Greater insurer accountability

For many motorists, these improvements could prove more valuable than a modest reduction in premium costs.

After all, the true value of insurance is revealed when a claim is filed and not when a policy is purchased.

What Should Vehicle Owners Do Before Their Next Renewal?

With the insurance landscape changing rapidly, consumers should become more proactive.

Before renewing your motor insurance policy:

Compare multiple insurers instead of auto-renewing.

Review claim settlement performance.

Check coverage for accessories and modifications.

Evaluate EV-specific add-ons if applicable.

Explore usage-based insurance products where available.

Keep an eye on the Bima Sugam rollout.

The cheapest policy isn't always the best policy.

Increasingly, value will be determined by coverage quality, claims support, and customer experience.

The CarBike360 Verdict

The biggest mistake consumers can make is focusing only on whether premiums will rise or fall.

The more important question is whether India's motor insurance market is becoming more transparent, competitive, and customer-friendly.

What's particularly notable is the timing. Insurers are being asked to modernize at the same moment that EV adoption, connected-car technology, and rising repair costs are changing the economics of vehicle ownership.

In many ways, IRDAI is preparing the insurance industry for the next generation of vehicles rather than the current one.

Premiums may not suddenly become cheaper. But if these reforms achieve their intended goals, Indian motorists could benefit from easier comparisons, faster claims, more personalized insurance products, and a significantly better ownership experience.

The real impact may not be what you pay next year.

It may be how motor insurance works for the next decade.

FAQs About IRDAI Motor Insurance Reforms

Will car insurance become cheaper in 2026?

Not necessarily. While IRDAI's reforms may improve competition and efficiency, rising repair costs and claim expenses could keep premiums elevated in the short term.

What is Bima Sugam?

Bima Sugam is a proposed digital insurance marketplace that will allow consumers to compare, purchase, renew, and manage insurance policies through a single platform.

What is usage-based motor insurance?

Usage-based insurance calculates premiums using factors such as mileage, driving behaviour, and vehicle usage patterns instead of relying solely on traditional risk categories.

How will IRDAI reforms affect EV insurance?

The reforms could encourage insurers to develop more specialized products for EV owners, including battery protection and customized coverage options.

Can safe drivers pay lower insurance premiums in the future?

Potentially yes. Telematics-powered and usage-based insurance products may allow insurers to reward safer driving habits with lower premiums.

You May Like

Find your perfect car

Budget

Brand

Body Type

Fuel

Mileage

More

Latest Car Videos

Other Car Articles

Main Title: Nissan Tekton vs 2026 Volkswagen Taigun Price Features and Engine Comparison

Nissan Tekton vs MG Astor: Detailed Comparison of Features Performance and Value

Tata Nexon EV vs Petrol Running Cost Comparison for Long Distance Travel

Nissan Tekton Visia Plus vs Acenta : Price, Features and Variants Compared

Listen to Car Audios